Weekly Blog #14

“You keep using that word. I do not think it means what you think it means.” Inigo Montoya, The Princess Bride

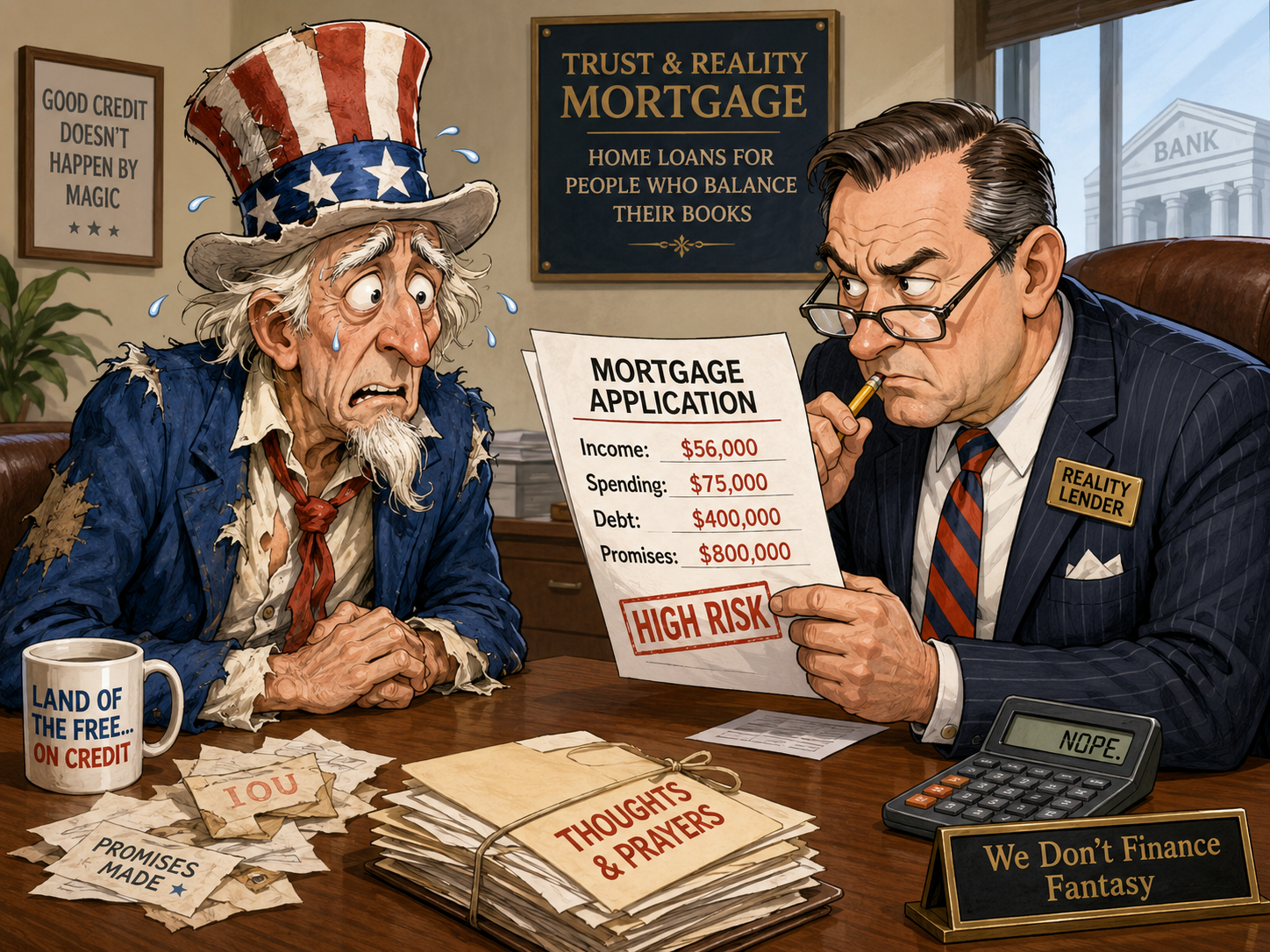

Word out of Washington is that the Trump Administration is considering whether to declare a national housing emergency. On the surface, the reasoning is understandable. Home prices have surged to record highs, mortgage rates hover near multi-decade peaks, and housing affordability is at its lowest point in forty years. Calling it a crisis resonates politically—millions of families feel locked out of the market, while renters confront rising costs and shrinking options.

But beware the word “emergency.” In politics, it rarely means what you think. Declaring an emergency is always a pretext for central planning; for Uncle Sam to interfere with free markets. History shows us that whenever government uses a crisis as a pretext for intervention, the results are never what voters are promised—and often exactly what markets fear.

We’ve been here before. The Clinton Administration in the 1990s identified a “housing crisis” of its own: stagnant minority homeownership rates and unequal access to credit. With HUD Secretary Andrew Cuomo leading the charge, the Administration leaned hard on Fannie Mae and Freddie Mac, the two government-sponsored enterprises (GSEs) that form the backbone of the secondary mortgage market.

Freddie and Fannie don’t make loans. Instead, they buy mortgages from banks and credit unions, bundle them into securities, guarantee those securities against default, and sell them to investors. This process—called securitization—frees up capital so lenders can make more loans. In theory, it promotes liquidity, stability, and affordability in the mortgage market.

The Clinton team saw this machinery as the key to expanding homeownership. Their solution? Loosen underwriting standards. Coerce Freddie and Fannie to buy more loans made to borrowers with little money down, sketchy credit histories, and/or unverifiable income. “Affordable housing goals” were written into the GSEs’ charters, and HUD ratcheted them higher year after year. By the late 1990s, Freddie and Fannie were under enormous pressure to buy, package, and guarantee ever-riskier loans.

By the mid-2000s, underwriting standards had been gutted. “No income, no job, no assets” (NINJA) loans were being churned out by originators and waved through by GSEs hungry to meet quotas. Investment banks gfollowed suit, flooding Wall Street with investment-grade mortgage-backed securities that were anything but.

We know how the story ends. When the housing bubble burst, defaults soared. Freddie and Fannie—once deemed too big to fail—collapsed into federal conservatorship in 2008, where they remain to this day. The “well-intended” policies of the Clinton era, turbocharged by subsequent administrations, laid the groundwork for the Great Financial Crisis.

The lesson is as old as economics itself: when government interferes with markets in the name of crisis management, it plants the seeds of the next crisis.

The bureaucrat’s crisis management playbook reads like this:

- Label a challenge an emergency.

- Expand federal authority in the name of fixing it.

- Relax standards or inject subsidies to engineer short-term relief.

- Leave taxpayers holding the bag when the unintended consequences appear.

- Claim free market failure and write thousands of pages of new regulations that promise to protect Americans from this sort of thing ever happening again.

It doesn’t matter whether the issue is housing, healthcare, student loans, the environment, or energy. Declare a crisis, override the market, and unintended consequences soon follow.

Economist Thomas Sowell put it bluntly: “There are no solutions, only trade-offs.” Policymakers rarely acknowledge this. By framing every policy as the cure to an emergency, they justify heavy-handed intervention while ignoring the knock-on effects.

Consider just a few examples from housing policy alone:

- Rent control, meant to protect tenants, often reduces supply and leads to worse housing stock.

- Zoning restrictions, meant to preserve neighborhood character, drive up prices by constraining supply.

- Subsidized mortgages, meant to help buyers, inflate demand but fail to increase supply.

Each intervention solves one problem and creates two more. Markets adapt. Builders shift capital to less regulated sectors. Lenders tighten elsewhere to offset loosened rules. Investors demand higher returns for higher risk. The cycle repeats.

If we really want to address the scarcity of housing in America, the answer is not another declaration of emergency. The answer is to let supply respond to demand. That means tackling the structural barriers that keep builders, investors, and entrepreneurs from meeting the market where it is.

- Streamline permitting–In many cities, getting approvals takes years. Every month of delay adds cost.

- Fix zoning–Outdated codes prevent duplexes, ADUs, and multi-family projects where they’re most needed.

- Cut fees and mandates–Impact fees, inspection costs, bonding requirements, and union-only labor rules bloat costs by 20–30%.

- End regulatory layering–Federal, state, and local rules pile on delays and legal fees, which ultimately show up in the sale price.

Remove those barriers, and you unleash builders. Capital will flow to housing the way it flows to any scarce good—because profit is a magnet. Declaring a crisis won’t make homes cheaper. Unleashing supply will.

The Trump Administration is right about one thing: America has a housing problem. Affordability is stretched, supply is constrained, and younger families are being priced out. But the temptation to declare a housing crisis should be resisted.

History shows that every time government declares an emergency to override markets, the cure is worse than the disease. The Clinton-era push to expand homeownership by dismantling underwriting standards didn’t solve a crisis—it manufactured the conditions for the worst financial collapse since the Great Depression.

The best way to solve the housing shortage is not more intervention. It’s less. Clear the thicket of regulations, fees, and restrictions that strangle new construction. Let builders build. Let capital flow. Let supply rise to meet demand.

Do that, and prices won’t fall because Washington declared them affordable. They’ll fall because the market created abundance from scarcity—not by executive decree but for a profit.

Mark Lazar, MBA

CERTIFIED FINANCIAL PLANNER™