“Give me control of a nation’s money and I care not who makes it’s laws” Mayer Rothschild

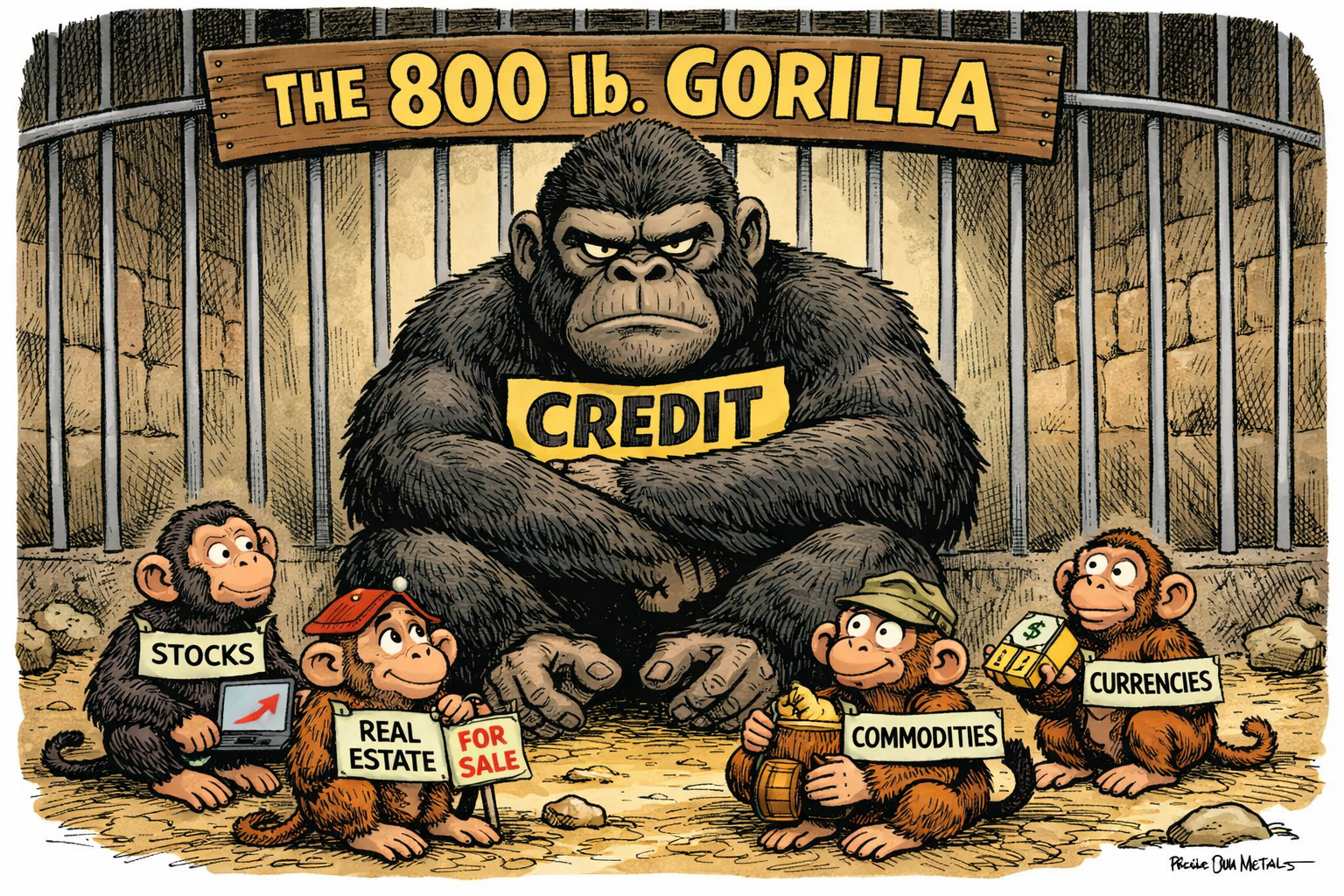

When most people say “the market,” they usually mean stocks. If they’re feeling speculative, maybe crypto. If they are in real estate, they’re probably thinking housing. But among the many markets that make up a modern economy; equities, bonds, real estate, commodities, currencies, derivatives, and digital assets, the credit market is arguably the most important. Why? Because credit prices capital, transmits monetary policy, and determines which projects get funded and which don’t.

To appreciate its importance, consider the size of the major U.S. markets; the stock market is $62 trillion, the bond market $50 trillion, and residential + commercial real estate over $65 trillion. In other words, we are talking about a financial system measured in staggering numbers. Yet despite the attention given to equities and housing, it is the credit market that quietly underpins much of it.

At its core, a functioning economy requires the factors of production: land, labor, capital, and entrepreneurship. Of those four, capital plays the enabling role. Land may exist, labor may be available, and entrepreneurial ideas may be abundant, but without capital, much of that potential remains dormant. Projects do not get financed. Businesses do not expand. Inventories are not built. Properties are not acquired or improved. Credit bridges that gap by moving savings from those with surplus capital to those capable of deploying it productively.

That function is central to economic growth. Credit supports investment, employment, and consumption. It allows long-duration assets to be funded over time rather than paid for entirely out of current income. In that sense, the credit market is not merely one market among many. It is the mechanism through which capital formation occurs. It is the connective tissue between savings and production.

The credit market also does something equally important: it establishes the price of money, time, and risk. Interest rates are not just arbitrary numbers on a screen. They are signals. A loan rate reflects some combination of expected inflation, real return requirements, liquidity conditions, duration, and perceived default risk. When those variables change, the impact ripples outward through the economy. Lower borrowing costs tend to encourage expansion and asset formation. Higher borrowing costs tend to slow them. Credit, therefore, acts as both accelerator and brake.

This is one reason the credit market often tells you more than the markets that get the headlines. Equity markets are highly visible, but they are also heavily influenced by narrative, momentum, and sentiment. Credit is usually more sober. Lenders and bondholders are not paid for optimism. They are paid for being repaid. As a result, credit instruments often embed a more disciplined view of risk, cash flow durability, and downside exposure.

For the attentive observer, credit markets provide an extraordinary amount of information. Treasury yields reveal expectations regarding inflation, growth, and the future path of monetary policy. Credit spreads reveal the market’s perception of financial stress and default risk. Mortgage spreads provide insight into housing finance conditions, liquidity, and prepayment expectations. The shape of the yield curve tells its own story. A steepening curve implies one set of expectations; a flat or inverted curve implies another. Each of these signals matters.

The U.S. Treasury market occupies a particularly important role in this framework. It remains the deepest, most liquid, and most actively traded fixed-income market in the world, and it serves as the benchmark from which countless other assets are priced. Corporate bonds, mortgage-backed securities, commercial real estate loans, and even equity valuations are influenced, directly or indirectly, by Treasury yields. If you want to understand the price of capital in the broader economy, start with the risk-free curve. Then look at spreads.

That is where the credit market becomes especially revealing. The spread between Treasuries and investment-grade corporate debt tells you one thing. The spread to high-yield debt tells you another. The pricing of mezzanine debt relative to senior secured debt tells you something else again; it is a market-based estimate of duration, liquidity, collateral quality, and borrower risk.

This is also why credit markets tend to be more efficient than many investors realize. Participants in these markets are generally less concerned with potential gains and more concerned with repayment capacity. They analyze debt-service coverage, collateral protection, maturity profiles, covenant packages, and recovery value. Their orientation is toward downside discipline, not optimism. That makes credit particularly useful as a diagnostic tool because it forces a more rigorous assessment of reality.

In practical terms, that matters because nearly every major economic outcome depends, at least in part, on the willingness of lenders and investors to extend capital. When credit is abundant and attractively priced, economic activity tends to accelerate. When it becomes scarce, growth slows, regardless of how optimistic other markets may appear. For that reason, the credit market is not merely a reflection of economic conditions. It is a leading determinant of them.

Equities matter. Housing matters. Commodities matter. Currencies matter. But credit sits at the center of the system because it governs the terms under which capital is created, deployed, and repriced.

In summary, if you want to understand the true pulse of the economy, learn to speak credit. Because while other markets get the spotlight, credit is the market that quietly determines what is possible.

Mark Lazar, MBA

CERTIFIED FINANCIAL PLANNER™