Weekly Blog #14

“Price is what you pay. Value is what you get.” Warren Buffett

June’s commentary, What’s It Worth?, looked at the many ways real estate can be valued—from comps and replacement cost to cap rates and discounted cash flows. But one critical concept I didn’t cover is the principle of highest and best use. In real estate, this principle often explains why two properties with the same square footage, location, and construction quality can have very different values.

At its core, highest and best use is the most profitable legal use of a property, considering what is physically possible, financially feasible, legally permissible, and maximally productive.

In practice, this means a property is not always worth the most in its current configuration. Sometimes, the way to maximize value is to reimagine the property entirely.

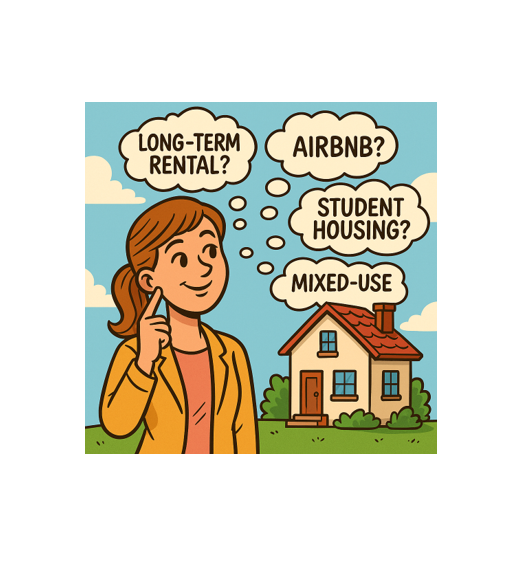

Take, for example, a 4,000 square foot, five-bedroom home in Utah County. As a single-family residence, it might appraise for ~$900,000. But what if zoning allowed it to be repurposed as a short-term rental, student housing, or even a mixed-use commercial property? The value proposition changes dramatically. What was once “just” a family home could suddenly produce income streams that justify a much higher valuation.

Savvy investors know how to look beyond the surface and ask: What else could this property be?

The concept of highest and best use has always mattered, but it is especially relevant in today’s environment. The housing shortage has become the crisis du jour, with demand far outstripping supply across much of the country.

City governments, under pressure to address affordability, are more willing than ever to revisit and rewrite local rules, ordinances, and zoning codes. For developers and investors, this creates opportunity. A parcel once restricted to low-density single-family housing might now be eligible for townhomes, accessory dwelling units (ADUs), or even multi-family apartments.

The potential for zoning reform means that properties previously locked into one use may suddenly have much higher and better alternatives. For those who can see around corners—and navigate the political process—there is value waiting to be unlocked.

Highest and best use isn’t just about what you could do with a property—it’s also about the cost of not doing it. This is where the principle of opportunity cost comes into play.

Imagine you purchase a home with a separate guest quarters. Your plan is to rent it out for $1,500 a month. But life gets busy, and you never get around to listing it. Twelve months go by. You’ve left $18,000 on the table. That’s the opportunity cost of inaction.

Put another way: it’s like stepping over fifteen $100 bills every single month and leaving them on the sidewalk. Time really is money.

Opportunity cost applies on the institutional level too. A bank that owns underutilized land, a city that blocks redevelopment through outdated zoning, or an investor who sits on vacant property all face the same issue: the real cost of doing nothing can be enormous.

A few practical examples illustrate how powerful this principle can be:

- Urban Infill: A one-acre lot in a downtown corridor might support a $500,000 single-family home. But if rezoned for multi-family, that same parcel could hold a 20-unit apartment building worth $5 million.

- Adaptive Reuse: Old warehouses in Denver and Salt Lake City have been converted into trendy office spaces, breweries, or loft apartments — often multiplying their value several times over.

- Short-Term Rentals: A property in a tourist-heavy market may generate double or triple the cash flow as an Airbnb compared to a traditional long-term lease.

- Mixed-Use Development: Retail on the ground floor, apartments above — a combination that extracts more value than either use alone.

In each case, the key was seeing past the current use and unlocking the property’s true potential.

Of course, highest and best use has boundaries. Just because something is theoretically profitable doesn’t mean it’s achievable. You must consider:

- Legal Permissibility: Zoning, covenants, and building codes can restrict options.

- Financial Feasibility: Not every idea pencils out once you factor in construction costs, financing, and absorption risk.

- Market Demand: Building luxury condos in a market that only supports workforce housing is a recipe for losses.

- Community Pushback: Even if zoning allows, local opposition can derail projects.

Highest and best use is as much about navigating practical realities as it is about spotting opportunities.

Today’s environment of rising interest rates, tight supply, and shifting demographics makes this concept more relevant than ever. Investors who can creatively reposition assets will find opportunities others miss.

Meanwhile, governments looking to address housing shortages must recognize that the path to affordability lies in unleashing supply—not through more declarations of “crisis,” but by removing regulatory barriers that prevent property from reaching its highest and best use.

In real estate, value isn’t fixed. A property’s worth depends not just on what it is today, but on what it could be tomorrow. Highest and best use is the lens that brings that future into focus.

Pair it with the principle of opportunity cost, and the lesson is clear: doing nothing has a price. Whether you’re an individual homeowner overlooking rental income, or a city sitting on outdated zoning laws, inaction means leaving money—and opportunity—on the table.

The investors who thrive in this market will be those who can see past the present and reimagine the possible. Because the real value of real estate lies not in its current form, but in its highest and best use.

Mark Lazar, MBA

CERTIFIED FINANCIAL PLANNER™