OCTOBER 19, 2024

October 2024

Economic Alchemy

“We’re all Keynesians now.” Richard Nixon

Undergraduate econ students are typically introduced to several schools of monetary theory, such as Classical, Keynesian, and Modern—although in good conscience I hesitate to refer to the last one as a legitimate academic theory. Here’s a quick summary of each:

- Classical Theory–Milton Friedman was a leading advocate of Classical Monetary Theory (CMT), which states that prices are determined by the balance of supply and demand. Classical economists argue that if the money supply grows faster than output (the very definition of inflation; inflating the money supply), price levels will rise.

- Keynesian Theory–John Maynard Keynes proposed that policymakers could actively manage the economy by manipulating interest rates and the money supply. Prior to Keynes, the prevailing approach was laissez-faire, which allowed markets to self-correct. His theories, however, gave bureaucrats permission to abandon the gold standard, deficit spend, and print money to influence economic outcomes.

- Modern Monetary Theory–MMT contends that sovereign governments that issue their own currency can never run out of money because they can always print more. This fantastical notion has gained traction with some contemporary policymakers, such as Jared Bernstein, President Biden’s lead economic advisor, who attempts to explain his views in the following video.

One of Keynes’ central ideas was a concept that he referred to as the multiplier effect. In a nutshell, during economic downturns, he argued, the government should borrow money and inject it into the economy via demand-side spending schemes. Examples include the Inflation Reduction Act, Cash for Clunkers, and American Recovery and Reinvestment Act. Keynes suggested that for every extra dollar spent by the government, there was a $1.50 to $2.50 increase in total spending. If true, the multiplier effect was the magic economic elixir policymakers had been seeking.

From 1921 to 1930, the US ran a budget surplus of roughly 1%, with annual economic growth around 2%. By the end of the Depression, deficits exceeded 3%, yet the economy experienced negative economic growth. Despite Keynesian recommendations for deficit spending, the U.S. didn’t officially exit the Depression until the start of the WWII—when virtually every boarded-up factory was reopened to support the war effort. If Keynes was correct, why did it take twelve years and a global conflict to revive the economy? Shouldn’t the massive deficit spending and its supposed multiplier effect have led to a faster recovery?

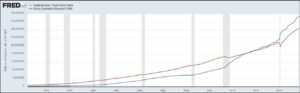

Between 1947 and 1969, the US ran a balanced budget. But starting in 1970, the government began to consistently run deficits. Since then, every president, with the exception of Bill Clinton between 1998–2001, has ran a budget deficit. Barack Obama effectively doubled the national debt during his eight-year term, increasing it from $10 to $20 trillion. Donald Trump added $8 trillion in just four years, and by the time President Biden leaves office in January, he will have matched that increase, adding another $8 trillion in debt.

US economic output has always far exceeded the national debt. However, in 2015 the lines crossed, and in nine short years, public debt now stands at over $35 trillion, or 46% higher than GDP. According to Keynes, deficits boost economic growth. But, despite record deficit spending, growth has fallen below the long-term average over the past nine years.

Keynes’ work was lauded by fellow academic elites, who had little or no real-world experience. However, it failed to account for a number of consequential factors, including diminishing returns, inflationary pressures (rising price levels), the crowding-out effect, sustainability of debt, inefficient allocation of resources, and currency valuation.

Keynesian theory gave legitimacy to imprudent fiscal policies, allowing profligate bureaucrats to claim the moral high ground. If the multiplier effect were real, recessions would be impossible as bureaucrats could simply spend their way to prosperity—the more they spend, the richer we are! Yet nearly a century of evidence demonstrates the opposite: deficit spending produces a fractionalization effect, where every dollar spent at the federal level grows the economy by some number less than one dollar

Akin to telling children that they can live on gum drops and cookies forever, Keynesian theory is a fairy tale for spendthrift politicians that excuses wasteful and irresponsible spending. Economic growth doesn’t come from piling on debt and printing money, but from innovation and advances in technology that enable companies to increase output with fewer inputs.

For nearly a century, western leaders been seduced by the Siren’s song of prosperity through endless spending, only to find ourselves buried under mountains of debt. Like the fabled King Solomon’s Mines, the promise of wealth through reckless fiscal policies is a perverse myth that has lured policymakers into actions ultimately leaving the world poorer. It’s time to declare Keynesian economics the failed experiment that it is and toss these theories into the scrapyard of bad ideas, doused in kerosene, and set on fire, never to return.

Mark Lazar, MBA

CERTIFIED FINANCIAL PLANNER™

wasatchfinance.com